Financial Controlling in a Multi-Entity Group: Why the Basics Break Down at Scale

Financial controlling did not stop working because the team got worse. It stopped working because the group got more complex - and the controlling architecture was never redesigned to match the new structure. The evidence accumulates in familiar symptoms: variance commentary that arrives after the decisions have already been made, KPI definitions that mean different things in different entities, and a month-end process that depends on one person's institutional knowledge and breaks whenever that person is unavailable.

The heroic consolidation: the most expensive finance risk most boards do not see

In most multi-entity groups that have not systematically rebuilt their controlling function, the group view is produced by one person - or a very small team - who manually assembles data from entity-level systems, applies adjustments that live in their own spreadsheet models, and produces a consolidated view that nobody else in the organisation could replicate independently. This person is typically effective. They are also a structural single point of failure.

The risk this creates is not hypothetical. A Deloitte study of finance function resilience across European mid-market groups found that 42% of multi-entity organisations had experienced at least one month-end close failure in the prior three years attributable to the departure or extended absence of a single controlling resource. The average close delay was 11 working days. The average cost - in management time, audit fees, and missed board deadlines - was EUR 180,000 per event.

An organic holding group, EUR 160M revenue, 6 entities across two markets, experienced this failure mode directly. The Group Controller departed for a competitor. The board discovered that month-end close - previously delivered reliably on day 12 - could not be replicated by the remaining finance team without the controller's undocumented Excel model. The model contained 34 manual adjustment steps, applied in a specific sequence, that translated entity-level ERP data into a consolidated group view. The close slipped to day 22 in the following month. The board pack contained numbers that differed from the statutory accounts by EUR 380,000 - a reconciling item that took four weeks to resolve. This was not a personnel problem. It was a controlling architecture that had never been documented, standardised, or made resilient to the departure of one person.

Four reasons controlling breaks down in multi-entity structures

Different charts of accounts across entities. Controlling requires comparability - the ability to compare Entity A's contribution margin against Entity B's on a like-for-like basis. When the two entities use different account codes for the same cost categories, comparability is structurally absent. Every analysis requires a manual translation step that introduces error and consumes time. Every variance explanation carries implicit uncertainty about whether the variance is operational or definitional.

KPI definitions that diverge after acquisition. EBITDA in the manufacturing entity may include depreciation on production assets that the SaaS entity does not carry. Gross margin in the services business may include consultant costs that the product business classifies as R&D. These are not accounting errors - they are legitimate differences in business model that have never been resolved at group level. The Group CFO receives an EBITDA bridge that combines incompatible definitions, and the variance commentary reflects genuine operational changes, definitional inconsistencies, and FX movements, all presented without labelling which is which.

Different close calendars and reporting cadences. Entity-level controlling runs at different speeds in different entities. Some close on day 5. Others close on day 15. A group controlling view assembled from inputs at different stages of completeness is not a group view - it is a patchwork of different moments in time, with the gaps filled by estimates. The estimates introduce error that compounds through the year and is never fully reconciled.

Controlling used as a reporting function rather than a management layer. A controlling function that produces monthly reports is retrospective. It describes what happened. A controlling architecture that surfaces variance triggers automatically, flags entity-level deviations from plan in real time, and drives escalation before the quarter is over is a management tool. Most multi-entity groups that have controlling have the former. The distinction is not academic - it determines whether finance influences decisions or explains them after the fact.

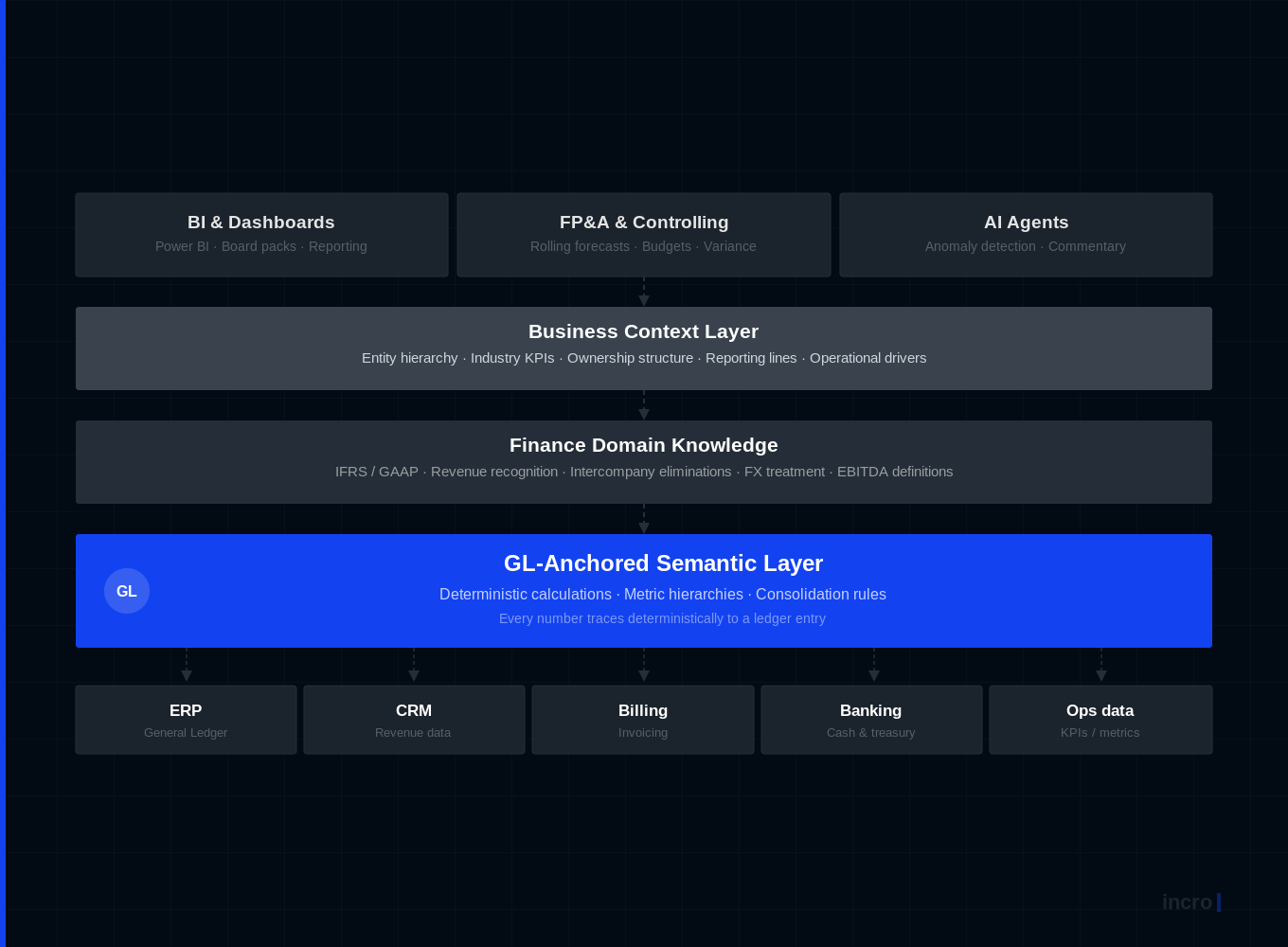

What group-level controlling architecture actually requires

Group controlling is not scaled-up single-entity controlling. It is a different design problem. Three structural components are non-negotiable before any controlling framework can function reliably at group scale.

A master chart of accounts enforced as a governance requirement. Not recommended. Not aspirational. Enforced - meaning every entity's ERP is configured to the group chart of accounts, deviations require Group CFO approval, and new entities are onboarded to the standard before their first consolidated close. This is the single most politically difficult requirement in group finance and the single most important technical one. Without it, comparability does not exist. With it, the entire controlling architecture becomes buildable.

Automated intercompany elimination as a system process. When IC elimination runs automatically - triggered by the data, not by a person with a spreadsheet - the group controlling view is available within hours of entity close, not days. The manual adjustment step that previously consumed the controller's first week of each month becomes a system check. The institutional knowledge that lived in one person's undocumented methodology becomes a documented, version-controlled configuration in the consolidation system. The risk of personnel departure ceases to be a close risk.

A consistent reporting calendar with enforced entity-level deadlines. Every entity controller knows when data is required and what format it must be in. The group controller's role becomes oversight, exception management, and analysis - not data assembly. This is the most immediately achievable of the three requirements and the most immediately impactful in reducing close duration.

The McKinsey benchmark: what finance functions that get this right achieve

McKinsey Global Institute research on finance function benchmarks across European mid-market groups identifies consistent performance differentials between groups that have invested in controlling architecture and those that have not. Groups with a unified chart of accounts, automated consolidation, and a consistent close calendar complete close an average of 8.2 working days faster than peer groups without these foundations. Finance team headcount per EUR 100M revenue is 32% lower. CFO satisfaction with reporting quality - measured by the frequency with which management accounts are presented without qualification to the board - is 2.4x higher.

These outcomes are not the result of technology investment alone. They are the result of architectural decisions - about data standards, process design, and governance - that precede any technology deployment. The technology executes the architecture. The architecture determines the outcome.

The controlling architecture as a strategic investment

For the Group CFO managing complexity across entities, the distinction between controlling as a cost and controlling as an asset is determined by architecture. A controlling function designed to produce monthly reports is a cost. A controlling architecture that embeds KPI triggers in operational data, surfaces entity-level deviations automatically, and delivers board-ready output within seven days of month-end is an asset that compounds in value as the group grows.

The investment in building that architecture is fixed. The return - through faster close, reduced finance headcount, earlier anomaly detection, and higher-quality board reporting - is ongoing. Groups that have made this investment consistently report that the payback period, measured against the current cost of the heroic consolidation they replaced, is less than 18 months.

If your group controlling view arrives too late to change the outcome it describes, or depends on institutional knowledge held by one or two people - talk to us about what rebuilding the architecture looks like for your specific structure.

Matt co-founded incro in 2020. Since then, he has worked with over 100 companies - from early-stage startups to PE-backed businesses across a wide range of industries.

He is an expert in corporate finance, FP&A set-up, and forecasting, and has built a reputation for turning complex financial functions into clear, board&investor-ready systems.

At incro, Matt drives company growth while designing the analytical frameworks and solutions that define how the firm delivers transformation — including co-creating CFO Studio, incro's AI-powered financial analysis platform.

He holds a degree from SGH Warsaw School of Economics and is the author of Methods and Procedures in the Assessment of Capital Investments (Difin, 2023), a rigorous framework for evaluating investment profitability, now used as an academic reference. Matt was named to the Forbes 30 Under 30 Poland list in 2025.

Your financial data won't fix itself.

30 minutes. We'll tell you exactly where your data is costing you money — and what AI can do about it.